Social Security Continues to Mistakenly Pay After Death of Parent

Whenever I'm asked about how Social Security survivor benefits work, I have a simple answer:

At death of the first spouse, surviving spouses receive the higher of:

- Their own monthly benefit, or

- The monthly benefit of the deceased.

That's the clean and straightforward answer, but it's not quite that simple. Although Social Security survivor benefits really are pretty simple, every family is different. Unique situations and variables can introduce some complexity.

Lump Sum Death Benefit

First, let's deal with the one-time payment formerly called a "funeral benefit." Upon the death of a Social Security beneficiary, the Social Security Administration pays a lump-sum death payment of $255. Needless to say, the $255 one time payment doesn't quite cover the cost of a funeral. It's been stuck at that level for several years and inflation has significantly eroded its useful value.

There are three categories of people who may receive the death payment:

- A surviving spouse, who was residing with the deceased spouse, or

- A surviving spouse, who was not residing with the deceased, but was receiving benefits based upon the work record of the deceased spouse, or who becomes eligible for benefits after the death of the spouse, or

- A surviving child, who was receiving benefits based upon the work records of the deceased parent, or who becomes eligible for benefit after the death of the parent. The payment is divided evenly among all eligible children.

If there are no eligible survivors in either of these three categories, then no death benefit is paid.

Even though $255 isn't a lot, who wants to pass on money that's rightfully theirs? If the eligible spouse or child is not receiving benefits at the time of death, they must apply for benefits within two years in order to receive the death payment.

Who Is Eligible For Spouse Survivor Benefits?

Many surviving spouses are eligible for monthly benefits from Social Security, based upon their age, disability, children at home, or some combination thereof. In general, spouse survivor benefits are available to:

- Surviving spouses, who were married at least 9 months, beginning at age 60. Benefit amount may depend on the age at which you file for benefits. Note: there are multiple exceptions to the 9 month requirement.

- Disabled surviving spouses, who were married at least 9 months, beginning at age 50. Benefit amount may depend on the age at which you file for benefits. Note: there are multiple exceptions to the 9 month requirement.

- Surviving spouses, of any age, caring for the deceased's child aged 16 or younger or disabled.

- Former spouses, who were married at least 10 years, beginning at age 60. Benefit amount may depend on the age at which you file for benefits.

Calculating the Benefit Amount

Figuring out how much you'll receive in Social Security survivor benefits requires a little math. The simple explanation is that at the death of the first spouse, surviving spouses receives the higher of their own benefit, or the benefit of the deceased. But this simple explanation doesn't consider (a) what age the deceased filed for benefits, if they did at all, and (b) when the surviving spouse decides to file.

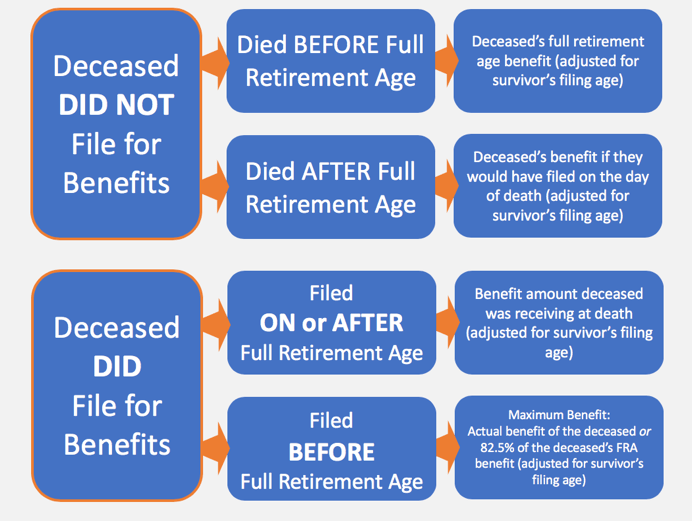

If the Deceased DID NOT File for Benefits

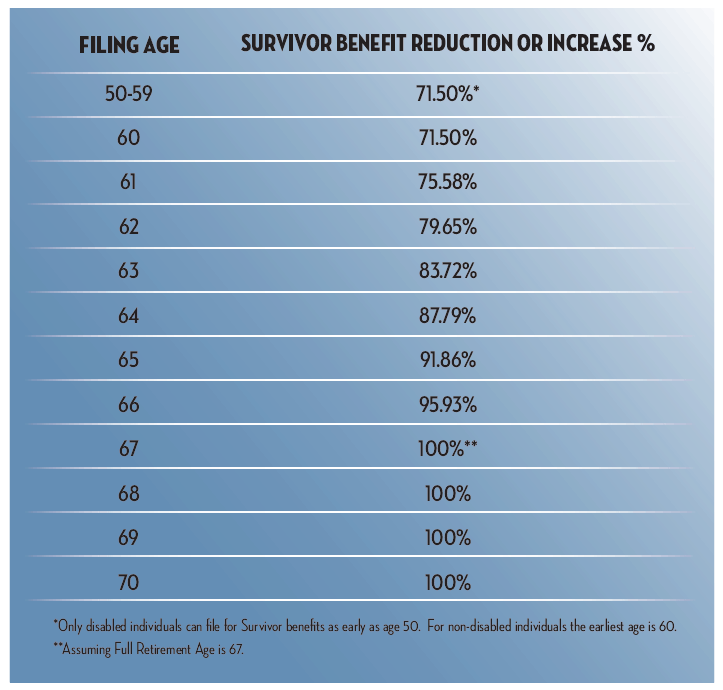

If the deceased spouse never filed for benefits, but died on or before their full retirement age, the calculation is relatively easy. The survivor receives the deceased's full retirement age benefit, adjusted for the survivor's filing age (see chart below).

If the deceased spouse never filed for benefits, and died after their full retirement age, the survivor receives the deceased's benefit in the same amount it would have been on the date of the deceased's death (including delayed retirement credits) reduced for the filing age of the survivor. You can see the next chart for more information on age-based reductions that come into play in both cases.

But what if the deceased spouse filed for benefits before he passed away? If this is the case, it could get a little more confusing.

If the Deceased DID File for Benefits

If the deceased spouse filed for benefit on or after their full retirement age, and the surviving spouse is at full retirement age, the benefit amount payable to the survivor will remain unchanged. If the surviving spouse is less than full retirement age, the amount the deceased spouse was receiving would be reduced by the filing age of the survivor.

If the deceased filed for benefits before their full retirement age, the surviving spouse is entitled to the full retirement age benefit of the deceased (reduced for survivors filing age) but will always be limited to the larger of the actual benefit of the deceased or 82.5% of the deceased's full retirement age benefit.

This 82.5% limit is a special rule often called the "Widows Limit" but the technical name is the RIB-LIM. It's meant to offer some protection for surviving spouses when the deceased spouse filed at, or near, the earliest age possible. This rule states that if your deceased spouse filed early, you'll be forever limited to either the amount they were drawing, or 82.5% of their full retirement age benefit. This rule has been a real lifesaver for some widows!

When it doesn't pay to delay

Here's where this gets really interesting. If your deceased spouse filed early for benefits, and you are also under full retirement age, there may be no reason to delay your filing beyond a certain age. It may be possible that your survivor benefit will not increase beyond your age 62 and 9 months!

For example, let's assume Jim's full retirement age benefit was $2,000. However, he filed at 62 and began receiving and age-based reduced benefit of $1,500. He died two years later. Because of his early filing, the most his surviving spouse will receive is the greater of his actual benefit ($1,500) or 82.5% of his full retirement age benefit ($2,000 x 82.5% = $1,650).

Based on the reductions for her filing age, she'd hit the 82.5% ($1,650) of his benefit right in between age 62 and 63. Once she was was at this age, there would be no benefit to continuing to delay filing for benefits. Further delay will not increase the survivors benefit!

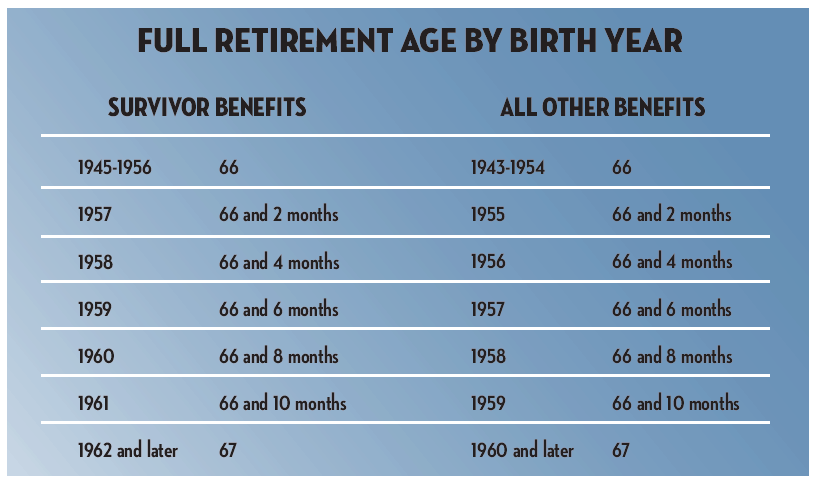

FULL RETIREMENT AGE FOR SURVIVOR BENEFITS

If you were born before 1962, you need to understand that the definition of "full retirement age" is different for survivor benefits than it is for all other benefits.

Knowing exactly when you are full retirement age is important when filing for your survivor's benefits. Why? Because if the survivor benefit is the highest benefit you'll be entitled to, there is generally no benefit to delaying your filing beyond that age.

Advanced Filing Strategies for Survivors

In early 2018 the Office of the Inspector General released a report with some shocking news. 82% of widows and widowers who are receiving Social Security survivors benefits are actually entitled to a higher monthly benefit payment. The only problem is, the SSA never made them aware of this. This affected an estimated 9,224 widows and widowers 70 and older who could have received an additional $131.8 million in Social Security benefits had they been told they could delay filing for retirement benefits until reaching age 70.

There's no need to wait for them to tell you about it…let's jump in right now.

Prior to 2016 there were several popular Social Security filing strategies that would allow an individual to file for certain benefits and later switch back to their own benefits. The benefit of this was to allow their own benefits to grow with the 8% per year delayed retirement credits (from chapter xx) However, law changes in 2016 did away with many of the Social Security filing strategies. The one that remains belongs to survivors and it can be powerful . Here's how it works.

If you have a benefit based on your own work history, it could make sense to file for a reduced survivor's benefit as early as 60. While you are drawing your survivor benefit, your own benefit grows every month you delay filing for it. Generally, these adjustments could grow your benefit by 77% from age 62 to age 70. At age 70, you simply switch back to your own benefit (which is now higher).

Let's say Paula has her own benefit of $1,500 per month that she could take at 67, her full retirement age. Her husband passed away and she is eligible for a survivor benefit of $1,200 per month. If she restricts her application to a survivor benefit only, she can collect benefits while letting her own benefit grow.

From age 62 to 69, she could receive $1,200 per month as a survivor's benefit. Once her own benefit has grown to the maximum, at age 70 and beyond, she can simply take that and receive $1,860 per month for the rest of her life.

The Social Security Administration discusses this strategy at this link.

Earnings Limit On Survivor Benefits

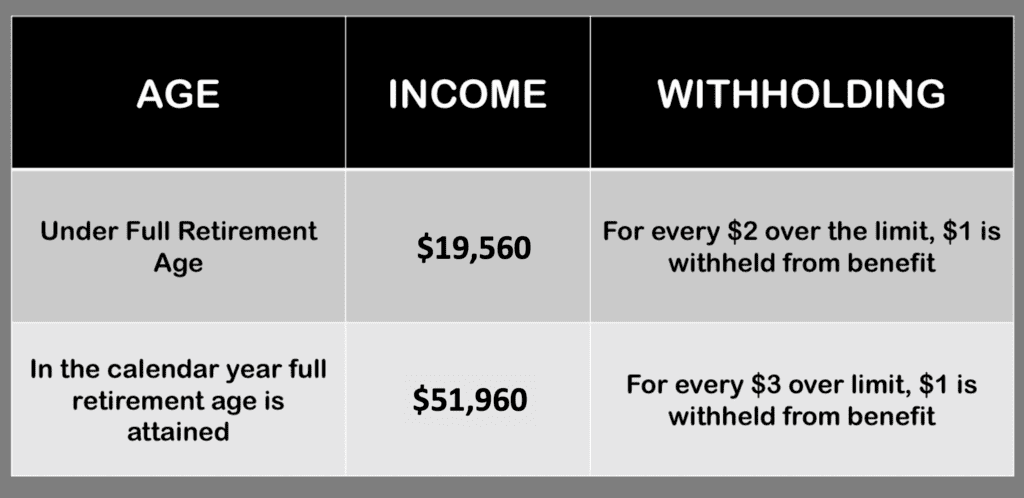

If you file for any Social Security retirement benefit (your own, spousal or survivor's) before your full retirement age, there is a limit to how much you can earn. The fact that this also applies to survivor benefits will often catch individuals by surprise.

If you are under full retirement age you are limited to $19,560 in wages or net earnings from self employment. If you exceed that limit, your benefit will be reduced by $1 for every $2 you go over. The one exception is the calendar year you turn full retirement age. For that period, your limit is a much higher $51,960. The amount they'll reduce your benefit by is more generous as well.

Once you are full retirement age, there is no limit to the amount you can earn while drawing Social Security. You can read my article on the Social Security earnings limit or watch my video.

NOTE: Although the SSA uses a slightly different table for determining FRA for survivor benefits, the earnings limit is always tied to FRA for retirement benefits.

Benefits Available to Children & Parents

Eligible spouses aren't the only ones that can receive Social Security survivor benefits. Dependent children and parents may also be entitled.

If you want to learn more, here are the best resources on the topic:

Children's Benefits:

Social Security Benefits for Children: The 4 Most Important Things You Should Know

Social Security Benefits for Grandchildren

Parent's Benefits

Social Security Benefits for Dependent Parents -Article by Mike Piper, the author of "Social Security Made Simple."

How To Claim Survivor's Benefits

To begin receiving survivor's benefits, you must make a claim with the Social Security Administration. Survivor's benefit's claims may not be made online. You can start the claims process over the telephone,1-800-772-1213, or go to your local Social Security office. Making an appointment may reduce your wait time.

The death should be reported to the Social Security Administration as soon as possible. In many cases, the funeral home can make that notification. You will have to provide the funeral home with the deceased's Social Security number.

Documents To File A Social Security Survivor Claim

The Social Security claims process may require the following documents. While each document may not be required, it is easier to come prepared than to have to make several trips or follow-up appointments.

- Proof of death—either from a funeral home or death certificate;

- Your Social Security number, as well as the deceased worker's;

- Your birth certificate;

- Your marriage certificate, if you are a widow or widower;

- Dependent children's Social Security numbers, if available, and birth certificates;

- Deceased worker's W-2 forms or federal self-employment tax return for the most recent year; and

- The name of your bank and your account number so your benefits can be deposited directly into your account.

If you don't have all the documents you need, start the claims process anyway. In many cases, your local Social Security office can contact your state Bureau of Vital Statistics and verify your information online at no cost to you. If they can't verify your information online, they have other ways to help you get the information you need.

Questions?

If you still have questions, you could leave a comment below, but what may be an even greater help is to join my FREE Facebook members group. It's very active and has some really smart people who love to answer any questions you may have about Social Security. From time to time I'll even drop in to add my thoughts, too. Also…if you haven't already, you should join the 100,000+ subscribers on my YouTube channel!

Source: https://www.socialsecurityintelligence.com/social-security-survivor-benefits-and-death/